If you’re a real estate agent near a military base — and you likely are since California is home to dozens of military bases — you’ve probably had the privilege of assisting a military family buy, rent or sell a home.

Serving in the military usually means moving within a couple years of arriving in a new community. Turnover is high and time is especially important when buying and selling. It’s a challenge for military homeowners. Agents assisting military homeowners share in the challenge, but have the opportunity to develop expertise in a niche market with a great referral base.

In most cases, a homebuyer needs to reside in their home for two-to-five years (depending on the location) for owning to make more financial sense than renting, mostly due to transaction costs. In California’s largest military populace — San Diego — the average breakeven horizon when buying makes more sense than renting is 3.8 years.

Therefore, to avoid losing money on a home purchase, a military homebuyer in San Diego either has to:

- bet on getting reassigned to the same duty station at the end of their current (usually two-year) tour; or

- plan to rent their home out after they move.

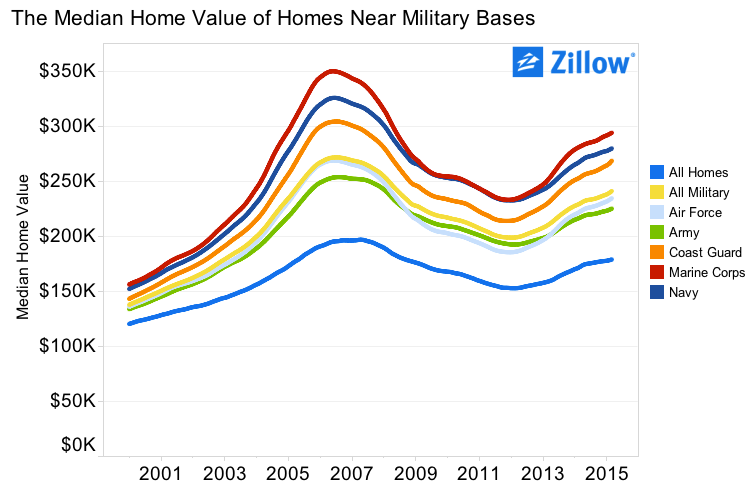

San Diego military families also have it hard when it comes to home prices. The median home value near military bases is $588,000, according to Zillow. This is 24% higher than the San Diego County average media home value of $475,000.

This same analysis shows home prices are more volatile near military bases regardless of the location:

Source: Zillow

How do military bases support home prices?

Given the hardships and uncertainty of homebuying as a member of the military, how do home prices stay significantly elevated in areas dependent on a large military population?

It’s possible the high turnover rate of military homebuyers — on top of the reliable income provided by military jobs — give home prices an extra boost.

Further, each active duty military member receives a basic housing allowance. The housing allowance acts as a subsidy inflating local home prices.

Basic housing allowance amounts are based on the servicemembers’s duty location, pay grade and whether or not the member has dependents. This housing allowance is meant to cover a family’s housing expenses typical to the area. The housing allowance is usually adjusted annually, based on changes in the local economy.

Current housing allowance amounts are available here.

This housing allowance is a helpful yardstick, and not just for military homebuyers. It’s also used by military homebuyers-turned-landlords when they move away from their duty stations.

For example, when a military family finds out they are scheduled to move, finding a renter is as easy as contacting their network to find another military family that has orders to that duty station. Looking up the housing allowance gives the military landlord an easy way to determine how much rent to charge.

The agent’s role

Real estate agents in areas with large military populations ought to take advantage of the opportunities presented. These include serving as the:

- buyer’s agent for military families new to the area;

- property manager for families choosing to rent out their homes when they move away; and

- seller’s agent when the military family eventually sells.

Since military turnover is continuous, make sure you let current military clients know you’re happy to help their military colleagues who are new to the area. The military community is tightly knit. One military referral goes a long way.

Having trouble getting your foot in the door? Try these steps:

- familiarize yourself with the ins-ands-outs of U.S. Department of Veterans Affairs (VA) mortgages;

- advertise your willingness to work with military families on your real estate website and marketing materials; and

- specify that you are a relocation specialist for active-duty military.

Are you already “in” with the military community? What are your tips? Share them in the comments!

Related article:

{kind=link}