This form is used by a vacation rental operator when entering into an employment agreement with an absentee vacation rental owner for the management of a vacation rental property, hotel, motel, inn, boarding house, lodging house, tourist home or similar transient accommodations for periods of 30 days or less, to document the duties of the manager and obligations of the vacation property owner under the employment.

Transient occupancy

Transient occupancy is the occupancy of a vacation property, hotel, motel, inn, boarding house, lodging house, tourist home or similar sleeping accommodation for a period of 30 days or less. This type of occupant is classified as a guest or a transient occupant. A transient occupant/guest is not a tenant and has considerably different legal standing and obligations. Thus, a transient occupancy is not controlled by landlord/tenant law.

A guest occupies property known as lodging, an accommodation or a unit. In the context of transient occupancy, the property is never described as a space or premise(s). Further, the property is not called a rental property. The term “rental” implies a landlord/tenant relationship exists, which it does not, between a guest and owner of the property.

The guest’s occupancy is labeled a stay, not possession which is exclusive to a tenant. During a guest’s stay in the lodging, the owner or manager of the property is entitled to enter the unit at check-out time even though the guest may not yet have departed. In contrast, a landlord is not permitted to enter a tenant’s unit without proper written notice when the tenant has not yet vacated.

Employing a manager

A property manager who manages “vacation rental” accommodations needs to maintain detailed accounting records. This is the case whether the manager is employed by an owner of a:

- single family residence (SFR);

- unit in a common interest development (CID);

- unit in an apartment complex; or

- any other residence subject to a local transient occupancy tax.

Further, the property manager needs to send a monthly accounting statement to each landlord they represent and make the records available for inspection and reproduction by the owner. They also need to comply with the local transient occupancy taxing agency regarding collection, payment and record keeping. [CC §1864]

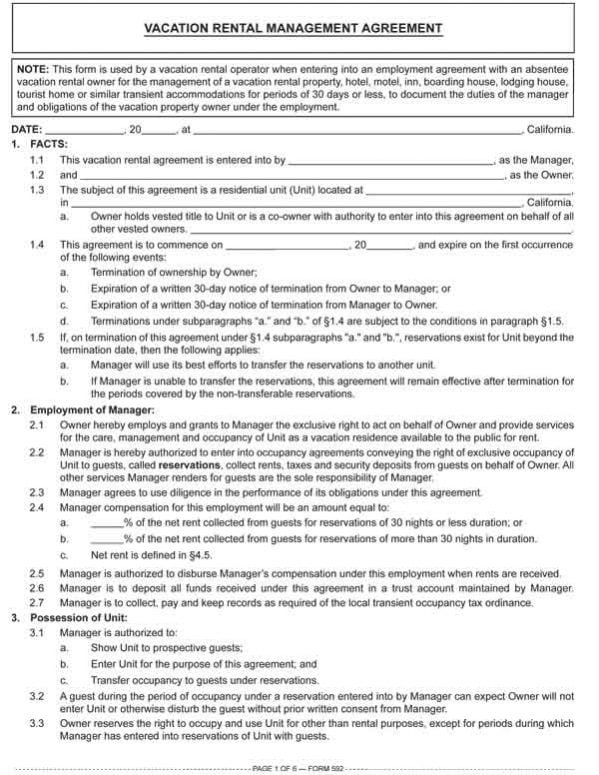

The Vacation Rental Management Agreement published by RPI is used by a vacation rental operator when entering into an employment agreement with an absentee vacation rental owner for the management of a vacation rental property, to document the duties of the manager and obligations of the vacation property owner under the employment. [See RPI Form 592]

Use of a Vacation Rental Management Agreement also formalizes the relationship between the vacation rental owner and the property manager. Specifically, the agreement presents:

- the employment commencement date and expiration terms;

- the manager’s duties, obligations and services; and

- the owner’s duty to maintain the unit. [See RPI Form 592]

Property manager’s self-help to remove guests

To remove a guest who fails to timely depart the unit and remains after a demand to leave the unit by the owner or manager has been made, the manager may intervene to remove the guest, a solution called self-help. If the manager’s self-help intervention might cause a breach of the peace, the manager is then to call the police. Without the need for a court order, the police or the sheriff will assist to remove the guest and prevent a danger to persons or property during the re-keying, removal of possessions and cleaning of the unit for the arrival of the next guest. [Calif. Penal Code §602(s)]

Transient occupancies include all occupancies that are taxed as such by local ordinance or could be taxed as such by the city or by the county.

Taxwise, the guest occupancy is considered a personal privilege, not a tenancy. Time share units, when occupied by their owners, are not transient occupancies and are not subject to those ordinances and taxes. [Calif. Revenue and Taxation Code §7280]

Transient units do not include residential hotels since the occupants of residential hotels treat the dwelling they occupy as their primary residence. Also, the occupancy period of most individuals in residential hotels is for more than 30 days.

Form updated 10-2016 to include the Form Description at the top, white header/footer convention and RPI branding.

Form navigation page published 10-2016.