Form-of-the-Week: Buy-Versus-Rent After-Tax Analysis – Form 320-4

Determining the financial benefits of homeownership

Renters become homeowners for many reasons. However, deciding whether they are better off financially by renting or buying a single family residence (SFR) is far more involved than just comparing their monthly rent payment against their proposed mortgage payment.

For real estate agents, one convincing tool readily available for use in a discussion with prospective homebuyers is preparing and reviewing visual evidence of the financial benefits generated by homeownership.

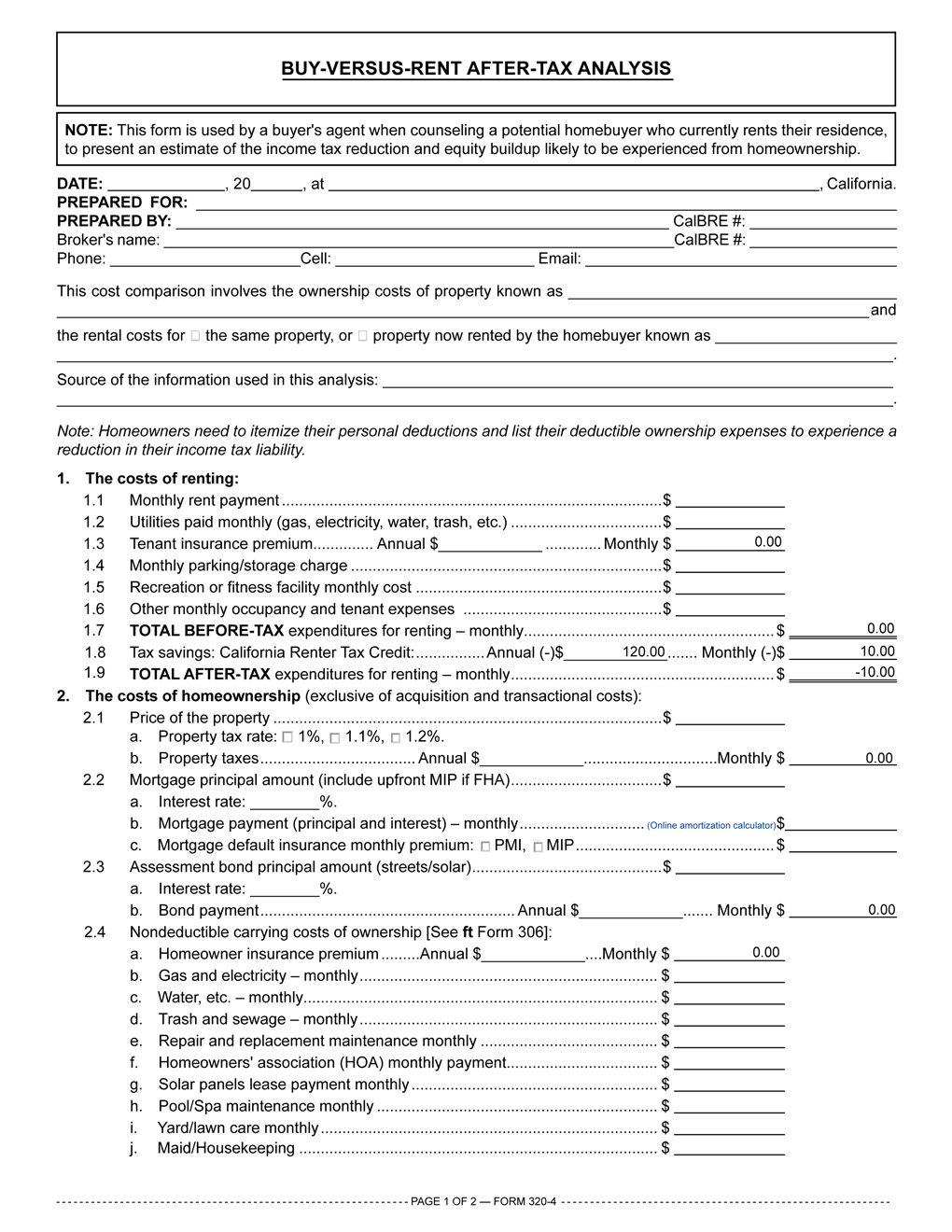

The Buy-Versus-Rent After-Tax Analysis – Form 320-4 — published by RPI (Realty Publications, Inc.) — is used by a buyer’s agent when counseling a potential homebuyer who currently rents their residence. It presents an estimate of the income tax reduction and equity buildup they are likely to experience from homeownership. [See RPI Form 320-4]

The Buy-Versus-Rent After-Tax Analysis form succinctly outlines how to efficiently compare monthly costs of renting versus owning for your buyer. The presentation includes mortgage interest deductions, tax savings and equity growth achieved based on your buyer’s home price, down payment and tax bracket. All comparative data are presented in the form as monthly and annual figures that buyers will quickly comprehend. Further, the form performs all the critical calculations for you.

The Buy-Versus-Rent After-Tax Analysis compares the future homebuyer’s current costs of renting against likely homeownership costs (and savings) and presents them in before-tax cash expenditures and after-tax results. [See RPI Form 320-4]

Related article:

Talk subsidized homeownership openly – hard numbers convert tenants to buyers

Preparing the Buy-Versus-Rent After-Tax Analysis

The following instructions are for the use of the Buy-Versus-Rent After-Tax Analysis. Each section of Form 320-4 has a separate analysis which is used to determine the final results.

Each instruction corresponds to the provision in the form bearing the same number.

1. The costs of renting: This section illustrates the total monthly cash outlay currently experienced renting shelter.

1.1 Enter the monthly rent payments.

1.2 Enter the month utility expenses, including gas, electricity, water and trash.

1.3 Enter the tenant’s renter’s insurance premium (calculated on a monthly basis).

1.4 Enter any monthly parking or storage charge.

1.5 Enter any monthly recreation or fitness facility charges.

1.6 Enter any other monthly occupancy and tenant expenses incurred.

1.7 The total monthly before-tax expenditures experienced by your buyer is automatically calculated.

1.8 The California Renter Tax Credit (defaulted to $120 per year or $10 per month) is automatically deducted from the total monthly before-tax expenditures to obtain the monthly total after-tax expenditures for renting displayed in provision 1.9. [See RPI Form 320-4 §1]

2. The costs of homeownership: This section illustrates the total monthly costs of homeownership the buyer of a property will likely experience (exclusive of the transactional costs of acquisition).

2.1 Enter the price of the property to be purchased and check the box to indicate the property tax rate (the annual property tax will automatically fill based on the price and rate).

2.2 Enter the mortgage principal amount and the upfront mortgage insurance premium (MIP) paid when the mortgage is insured by the Federal Housing Administration (FHA) (a link to an online amortization is provided), interest rate, mortgage payment, and check private mortgage insurance (PMI) or MIP if applicable;

2.3 Enter any assessment bond principal amount (e.g., street or solar), its interest rate and annual payment (the monthly payment will be automatically calculated).

2.4 (a – l) Enter monthly non-deductible carrying costs of ownership, itemized as homeowners insurance, utilities, repairs and maintenance, homeowners’ association (HOA) payment, solar panel lease payment and any other monthly home expenses. The total monthly nondeductible carrying cost of homeownership is automatically calculated.

2.5 Here, the total before-tax ownership expenditures (§2.1-2.4) is automatically calculated. [See RPI Form 320-4 §2]

3. Here, the before-tax difference in monthly expenditures of owning versus renting is automatically calculated. [See RPI Form 320-4 §3]

4. The monthly tax savings analysis: This section illustrates the total monthly after-tax expenditures for ownership.

4.1 (a – e) Here, the total monthly deductible ownership expenditures for mortgage interest, street/solar assessment bonds, PMI/MIP and property taxes is automatically calculated.

(f) Check the appropriate tax rate of the household.

4.2 Here, the monthly savings from reduced income taxes is automatically calculated.

4.3 Here, the total monthly after-tax expenditures of owning versus renting is automatically calculated. [See RPI Form 320-4 §4]

5. Here, the after-tax difference in monthly expenditures of owning versus renting is automatically displayed. [See RPI Form 320-4 §5]

6. Additional year-of-purchase tax savings for mortgage origination: This section illustrates the total deductible year-of-purchase tax savings for mortgage origination costs.

6.1 Enter the mortgage origination fees.

6.2 Enter the prepaid interest for month of closing.

6.3 Here, the total year-of-purchase mortgage origination deduction is automatically calculated.

6.4 Here, the household’s tax rate is automatically displayed.

6.5 Here, the additional one-time tax savings for year of purchase is automatically calculated. [See RPI Form 320-4 §6]

The second part of Form 320-4 presents the Buy-Versus-Rent Annual Summary based on the figures provided in the prior sections:

1. Before-tax:

1.1 Here, the total before-tax annual out-of-pocket difference between owning and renting is automatically displayed. [See RPI Form 320-4 Summary §1];

2. After-tax:

2.1 Here, the total after-tax out-of-pocket difference during first 12 months of ownership is automatically displayed.

2.2 The additional one-time tax savings for the year-of-purchase is automatically displayed.

2.3 Here, the total out-of-pocket difference during first 12 months of ownership is automatically displayed. [See RPI Form 320-4 Summary §2]

3. The wealth factor of home equity buildup:

3.1 Enter the mortgage principal reduction from amortization at 10 years. (Using the amortization schedule of a mortgage calculator, determine the principal balance remaining after 10 years. Then, subtract that figure from the original mortgage amount to determine the principal reduction.)

3.2 Here, the mortgage principal reduction as savings (10-year annual average) is automatically calculated.

3.3 Here, the home value increase (3.5% annual growth) is automatically calculated

3.4 Here, the total annual home equity buildup (10-year annual average) is automatically calculated. [See RPI Form 320-4 Summary §3]

4. Finally, the annual net financial benefit of homeownership versus renting is automatically calculated. [See RPI Form 320-4 Summary §4]

{kind=link}