Do you believe California needs another round of economic stimulus?

- No. (71%, 143 Votes)

- Yes. (29%, 58 Votes)

Total Voters: 201

Home prices are rising and homebuyers are impatient to purchase. Real estate professionals are eagerly shepherding the rapid buy-and-sell process along.

But how much of this excitement is built on solid economic principles (read: sustainable), and how much of it is just hot air?

Many of the economic successes of the past year can be traced back to government stimulus. No doubt, the authors of the past year’s stimulus programs intended to address both short-term needs and also set the economy on a path toward recovery. This long-term recovery is ultimately the goal of any injection of cash into the economy, one achieved through the multiplier effect of stimulus.

The multiplier effect is an economic idea that says the original input results in a larger output. In terms of government spending, the multiplier effect differs based on how dollars are spent. For example, for every dollar the government pumps into the economy, how much can we expect to see in return? When the multiplier effect is present, that dollar turns into many more dollars, expressed through rising incomes, greater spending and a higher gross domestic product (GDP).

The success of the economic multiplier effect can be broadly measured by the following formula:

Change in income / money supply

__________________________

Change in spending / injection of cash

The multiplier effect in practice

For example, consider the U.S. Federal Reserve and the money supply.

During the 2008 recession and long, drawn-out recovery years that followed, bank reserve balances skyrocketed. In total, reserve balances increased from $20 billion prior to the crisis to over $1 trillion in 2010. Corresponding with high reserves, the actual dollar amounts being lent (read: injected into circulation) plummeted.

This dynamic worried some economists, who were concerned that a shrinking base value of money circulating in the economy would result in a downward spiral in spending and negative inflation.

However, this analysis failed to take in the influence of demand. Instead, high reserve balances were found to have no impact on the level of bank loans, according to a 2010 Fed study.

In other words, the base value of the money multiplier — the amount of money spent or injected into the economy — is most influenced by demand.

The money multiplier in 2021

Unprecedented levels of cash injections have hit the streets in recent months. In 2020, the first round of individual stimulus payments was delivered to the bank accounts of the vast majority of Americans. This was followed by two more rounds of payments, amounting to $3,200 per adult and $2,500 per child thus far into the recession.

In response, household spending increased in the weeks following the receipt of each stimulus payment. On average, for each dollar received in stimulus, consumer spending increased by $0.25-$0.40. This was mostly spent on short-term goods, like food, and on debt payments, including rents, mortgage payments and credit cards, according to the National Bureau of Economic Research (NBER).

Further, this increased spending tapered off after just a few weeks of each stimulus injection. The individual payments have proven helpful for those struggling in the short term from the 2020 recession and job losses, but have made little impact on durable spending.

The reason directly corresponds with household expectations. Due to the economic uncertainty presented by the sudden shuttering of the economy in 2020, many households chose to stockpile nondurable goods, like food (not to mention toilet paper). The remainder of their money went to paying off debts and saving to stave off the potential for future job losses.

Quickly spent, the stimulus payments had a mellowing placebo effect on the economy. It made people feel better to have a little extra cash on hand, but this ultimately made little to no change in anyone’s long-term spending behavior.

When the stimulus runs out…

The multiplier effect of stimulus is greatly swayed by the mechanism of delivery. In practice, the stimulus payments made directly to individuals have provided a short-term boost to the economy. But, once spent, this money disappears into thin air.

In contrast, stimulus delivered through long-term vehicles of delivery will see a greater, long-term effect. This long-term impact allows the multiplier to take place.

One example of long-term stimulus is the recurring monthly child tax credit payments which begin in July 2021. Each eligible household — amounting to 88% of all households with children — will received monthly payments of $250-$300 per child, according to the Treasury Department. These monthly payments are meant to help families cover basic essentials for their children, but also to help pay for child care, essential for parents seeking to work.

Even better, any stimulus program that focuses on job creation will have multiplier potential. Access to stable, high-paying jobs will empower households to make larger, more durable purchases, thus supporting other jobs that rely on these long-term sources of income. However, stimulus programs focused on infrastructure and jobs have yet to become law.

For real estate professionals, the implications of the short-term nature of the last three rounds of stimulus are clear to see: the fuel tank is approaching empty.

With 1.7 million jobs still missing here in California — over half of those lost in 2020 — the housing market is on unstable ground. The market factors of historically low inventory and rapid price increases are deceptively optimistic. In fact, the housing market has been bolstered by several short-term efforts to prop up the market, including:

- three rounds of individual stimulus payments;

- the foreclosure and eviction moratoriums, which have kept jobless Californians housed throughout this recession and pandemic; and

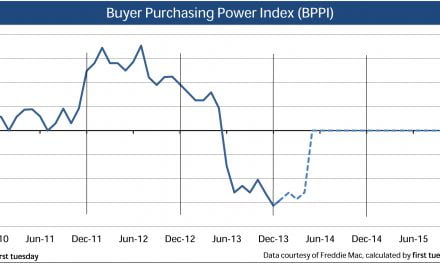

- record-low mortgage interest rates, which have boosted buyer purchasing power, enabling rapid price increases and a jump in refinance activity.

However, the moratorium on foreclosures and evictions is scheduled to end on June 30, 2021. Then, homeowners who are not in a forbearance plan and renters who have not come to an understanding with their landlords will lose their housing. Without the support of additional government money (another round of stimulus), evictions will rise and prices will fall.

The only long-term solution will be a return of jobs. This will occur more quickly through government-sponsored programs. Otherwise, jobs will eventually return organically. But at their current pace of recovery, jobs won’t even begin their return to pre-recession levels until around 2025.

Related article:

{kind=link}

STIMULUS, 5 TRLLION of DOLLARS will it help the real estate industry??? and more to come. The DOLLAR is loosing value as a result hard assets like oil and real estae are going up to protect agains the loss of value and unfortunately inflation is kicking in. Perhaps we should consider purchasing real estae as a protection because cash is loosing value. Interesting panorama.