Question:

What is the difference between reinstatement and redemption?

Answer:

When a lender begins foreclosure on a property, the property owner may terminate the foreclosure proceedings through reinstatement or redemption. Though they are similar, reinstatement and redemption are distinct concepts.

Reinstatement

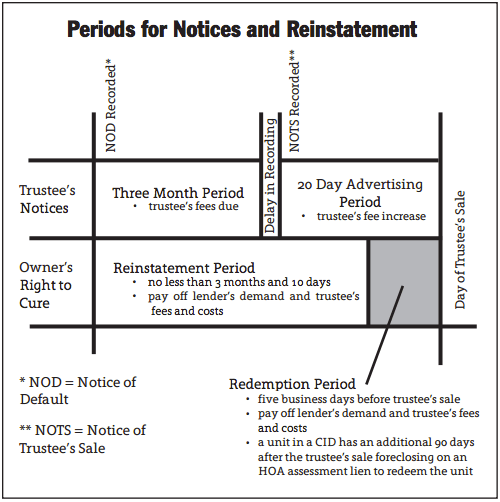

Reinstatement refers to a property owner or junior lienholder’s right to reinstate a mortgage and cure any default by paying the delinquent amounts due on the note and trust deed, plus foreclosure charges. [Calif. Civil Code §2924c]

After the notice of default (NOD) is recorded, the property owner or junior lienholder has up until five business days before the trustee’s sale to reinstate the trust deed, known as the reinstatement period. Since a trustee is required to wait three months after the recording of the NOD to post a Notice of Trustee’s Sale (NOTS) and an additional 20 days after the NOTS to commence the sale, the reinstatement period is approximately 105 days total.

Amounts due for reinstatement include:

- all delinquent amounts on the NOD, which consist of principal, interest, taxes and insurance (collectively known as PITI), assessments and advances;

- installments that become due and remain unpaid after the recording of the NOD;

- future advances made by the beneficiary after the recording of the NOD to pay taxes, senior liens, assessments, insurance premiums and to eliminate any other impairment of security; and

- costs and expenses incurred by the lender to enforce the trust deed. [CC §2924c(a)(1)

Upon reinstatement of the note and trust deed, the NOD is rescinded by the trustee and the recorded default is removed from the title to the property. [CC §2924]

Thus, after reinstatement, the owner continues ownership of the property as though the mortgage had never been in default.

However, the ability to reinstate a mortgage by curing a default is determined by the trust deed provision. Unless agreed to by the lender, some defaults prohibit reinstatement, requiring redemption instead. These include:

- a breach of a due-on clause;

- a waste provision; or

- a violation of law provision in the use of the property.

Redemption

If the default disallows reinstatement or if the property owner fails to cure a default before the reinstatement period expires, the property owner may redeem the property prior to completion of the trustee’s sale.

Redemption refers to a property owner or junior lienholder’s right to clear title to property of a trust deed lien by paying all amounts due on the note and trust deed, including foreclosure charges. [CC §2903]

Unlike reinstatement, the owner’s right to redemption runs until the trustee completes the bidding and announces the property has been sold. Any owner, junior lienholder or other person with an interest in the property may satisfy the debt and redeem the property prior to the completion of the trustee’s sale. [CC §2903]

Redemption requires the owner to pay:

- the principal and all interest charges accrued on the principal;

- permissible penalties;

- foreclosure costs; and

- any future advances made by the foreclosing lender to protect is security interest tin the property.

Ownership to the property is returned to the property owner only after all amounts due on the note and trust deed are paid in full.

Thus, to put it simply: reinstatement requires the payment of all delinquent amounts within the given reinstatement period, while redemption requires the property owner to fully pay all amounts before completion of the trustee’s sale.

Related article:

{kind=link}